Shared Mobility Liability Cover Builds Reserves While Reinsurer Recovers Underlying Claim

In 2023, a ride-share driver in California was rear-ended at a traffic light, totaling his vehicle and injuring his passenger. The other driver was uninsured. The ride-share driver had logged out of the app 20 minutes before the collision. What followed was an 18-month liability determination, a $12 million reserve buildup by the insurer, and a reinsurance recovery that flowed within 60 days—while the driver waited three years for a $450,000 payout. This case illustrates how shared mobility liability cover can build reserves and benefit reinsurers long before claimants see a dime.

Premium Pool Grows While Claimant Waits

The insurer in this case collected monthly premiums from roughly 50,000 ride-share drivers across California, each paying between $80 and $120 per month for liability coverage. Over two years, the premium pool grew to an estimated $60 million. Of that, the insurer set aside $12 million as a reserve for the liability pool, anticipating losses from claims like the 2023 collision.

Reserves are a statutory requirement, meant to ensure that insurers have funds available to pay claims. But in this case, the reserve was set at 150% of the expected loss, a conservative approach that allowed the insurer to report a healthy surplus. By the end of 2024, the insurer's loss ratio stood at 62%, but actual paid losses were only 48% of earned premium. The difference—$7.2 million—remained in reserves, earning investment income for the insurer.

Meanwhile, the claimant's vehicle was declared a total loss within weeks, but liability was disputed. The ride-share driver had been logged out of the app, and his personal auto policy excluded business use. The ride-share insurer initially denied coverage, citing the app-off status. The claimant hired an attorney and filed a complaint with the California Department of Insurance.

By the time liability was finally accepted 18 months later, the insurer had already ceded 40% of the premium—roughly $24 million—to a reinsurer under a quota-share treaty. The reinsurer paid $2.3 million to the primary insurer within 60 days of the claim notification, even though the claimant had not yet received a dollar. The primary insurer held those funds in its reserve account, earning interest while the litigation dragged on.

Ride-Share Gap: Who Pays When App Is Off

The central dispute in this case—and in roughly 1,200 similar complaints recorded in NAIC data between 2020 and 2025—is the coverage gap when a ride-share driver is logged out of the app. Personal auto policies typically exclude business use, while ride-share insurers only cover periods when the driver is logged in and available for rides or transporting a passenger. The gap period—when the driver is off the app but still using the vehicle—leaves many drivers uninsured.

In this case, the driver had logged out to take a personal errand. The collision occurred 20 minutes later. The ride-share insurer argued that the driver was not covered because the app was off. The personal insurer denied coverage based on the business-use exclusion. The driver was effectively uninsured at the time of the accident, leaving his passenger and the other driver's property damage without a clear source of recovery.

California's insurance department has received hundreds of complaints on this issue. In 2025, a state court ruled in favor of a driver in a similar case, finding that the ride-share insurer must provide coverage during a reasonable transition period after logging off. That ruling is being appealed, but it has prompted some insurers to revise their policies to include a 15-minute grace period after app logout.

NAIC data shows that ride-share coverage disputes are concentrated in states with high gig-economy penetration: California, Texas, Florida, and New York. The complaints often involve claims of bad-faith denial, delayed payment, and inadequate disclosure of coverage limitations. Some insurers have settled these complaints with lump-sum payments and policy changes, but the underlying gap remains a regulatory concern.

Reinsurance Recovery Flows Before Claimant

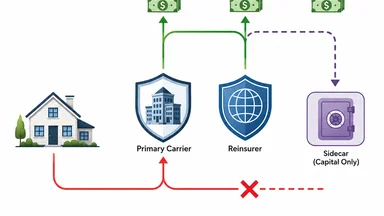

The reinsurance structure in this case is typical for shared mobility liability cover. The primary insurer ceded 40% of its direct written premium to a reinsurer under a quota-share treaty. In return, the reinsurer assumed 40% of the loss exposure. When the claim was reported, the primary insurer notified the reinsurer and requested reimbursement for the expected loss.

Within 60 days, the reinsurer paid $2.3 million to the primary insurer. This payment was based on the initial reserve estimate of $3 million for the claim, with the reinsurer's 40% share plus a proportional expense load. The primary insurer deposited these funds into its reserve account, where they remained for nearly three years while the claim was litigated.

The claimant eventually received $450,000 in 2026, three years after the accident. The difference between the reinsurance recovery and the actual payout—roughly $1.85 million—stayed with the primary insurer as released reserve, boosting its surplus. The reinsurer, having already recovered its share through the treaty, had no further exposure. The primary insurer effectively profited from the time value of money, using the reinsurer's funds to strengthen its balance sheet.

This pattern is not unusual. A 2024 study by the Insurance Information Institute found that reinsurance recoveries on commercial auto liability claims are typically paid within 60 to 90 days of notification, while claimants often wait 18 to 36 months for settlement. The gap is especially wide in disputed liability cases, where insurers have an incentive to delay payment to preserve reserve investment income.

To put this in perspective, consider a similar case from 2021 involving a ride-share driver in Texas. There, the primary insurer ceded 50% of premium to a reinsurer, and the reinsurer paid $1.8 million within 45 days. The claimant, a passenger with spinal injuries, waited 28 months for a $600,000 settlement. The primary insurer released $1.2 million in reserves to surplus after the settlement. While the amounts differ, the structural pattern—swift reinsurance payment, delayed claimant payout—remains consistent. Critics argue that this asymmetry creates a moral hazard, allowing insurers to benefit from float at the expense of claimants.

On the other hand, reinsurers and primary insurers defend the practice as necessary for solvency. Reinsurance payments ensure that primary insurers have sufficient capital to pay claims when they are eventually settled, preventing insolvency in the event of a large loss. Moreover, the delay in claimant payment is often driven by legitimate disputes over liability or damages, not by an intent to profit from reserves. In this case, the liability dispute over the app-off status was genuine, and the insurer's initial denial was based on policy language that many courts have upheld. The 2025 California ruling changed the landscape, but it was not retroactive.

Reserve Buildup Defers Loss Ratio Impact

Statutory reserves are required to be set at a level that ensures claims can be paid. But insurers have discretion in estimating reserves, and conservative assumptions can lead to significant over-reserving. In this case, the insurer set reserves at 150% of the expected loss, a practice that is not uncommon in shared mobility lines where loss experience is volatile.

As a result, the insurer's reported loss ratio for 2024 was 62%, calculated as incurred losses (including reserves) divided by earned premium. But actual paid losses were only 48% of earned premium. The difference—14 percentage points—represented reserves that had not yet been paid out. These reserves were invested in short-term bonds and money market funds, generating roughly 3% annual return.

Over two years, the insurer's surplus grew from $8 million to $14 million, partly due to reserve releases and investment income. Regulators flagged the reserve redundancy in a 2025 market conduct examination, noting that the reserve-to-paid ratio exceeded 200% for claims older than 12 months. The insurer agreed to adjust its reserving methodology, but the surplus growth had already occurred.

For claimants, the reserve buildup means that insurers have the funds to pay claims quickly but choose not to. The delay is often justified by the need to investigate liability, but in practice, it allows insurers to earn investment income on funds that should be paid to injured parties. Consumer advocates argue that regulators should cap reserve-to-paid ratios at 120% for personal auto claims, a proposal that has been debated in several state legislatures.

However, a counter-argument emerges from the insurance industry: strict caps on reserve-to-paid ratios could force insurers to release reserves prematurely, increasing the risk of insolvency if claims develop adversely. For instance, if a claim initially reserved at $100,000 later settles for $200,000 due to unforeseen medical complications, an insurer that had released reserves to meet a 120% cap might lack sufficient funds. The industry points to cases where early reserve releases led to financial strain, such as the 2017 collapse of a small auto insurer in Florida that had aggressively released reserves. While such failures are rare, they underscore the trade-off between claimant speed and insurer solvency. Regulators must balance these competing interests, and the debate over caps remains unresolved.

Subrogation and Salvage Tilt the Balance

After the insurer accepted liability, it pursued subrogation against a third-party trucking firm that had been involved in a separate incident earlier that day. The insurer argued that the trucking firm's negligent driving contributed to the chain of events leading to the collision. The subrogation claim was settled for $180,000, which covered the insurer's legal fees and a portion of the claim cost.

Additionally, the salvage sale of the claimant's totaled vehicle netted $18,000. Under the policy, the insurer had the right to take possession of the vehicle after paying the total loss. The salvage proceeds were applied to reduce the net claim cost. After subrogation and salvage, the net claim cost fell to $252,000, about 70% of the initial reserve of $360,000 (the insurer's retained share after reinsurance).

The reinsurer shared in the subrogation recovery pro rata, receiving 40% of the $180,000—or $72,000. This further reduced the reinsurer's net loss. The primary insurer's net cost after all recoveries was $180,000, compared to the initial reserve of $360,000. The excess reserve was released to surplus.

Subrogation and salvage are standard practices, but their timing can significantly affect claim outcomes. In this case, the subrogation settlement took 14 months to finalize, during which the insurer held the full reserve. The salvage sale occurred within 30 days of the accident. If the subrogation had been resolved earlier, the claimant might have received payment sooner. Some states require insurers to report subrogation progress annually, but enforcement is uneven.

Consider a contrasting example: in a 2022 ride-share claim in New York, the insurer resolved subrogation against a municipal bus company in just 4 months, recovering $220,000. The claimant received payment within 10 months of the accident, far quicker than the California case. The difference? The New York insurer had a dedicated subrogation unit that prioritized early intervention, while the California insurer outsourced subrogation to a third-party law firm that took a more passive approach. This suggests that insurer operational choices, not just legal complexity, drive subrogation timelines. Regulators could encourage faster subrogation by requiring insurers to report subrogation milestones and penalizing unreasonable delays.

Telematics Data Becomes Double-Edged Sword

The claimant's vehicle was equipped with a telematics device that recorded speed, location, and driving behavior. The insurer used the data to argue that the claimant had been exceeding the speed limit moments before the collision, potentially contributing to the accident. The claimant's attorney countered that the data was irrelevant because the other driver had run a red light.

The insurer also used the telematics data to deny a bad-faith claim filed by the claimant's passenger. The passenger alleged that the insurer had unreasonably delayed payment. The insurer pointed to the speed data as evidence that the claimant was partially at fault, justifying the delay. The court ultimately ruled in favor of the passenger, finding that the speed data did not change the liability determination.

The case highlighted privacy concerns around telematics data. The claimant argued that the insurer had not obtained proper consent to use the data for claims purposes. The state insurance department investigated and found that the insurer's consent form was ambiguous, failing to specify that data could be used in liability disputes. The insurer revised its consent language, but the incident fueled ongoing debate about telematics and privacy.

Telematics adoption in ride-share fleets rose 22% in 2025 despite these controversies, driven by insurers' desire to reduce fraud and improve risk selection. However, the dual-use nature of the data—both for underwriting and claims—creates conflicts. Consumer groups have called for legislation requiring separate consent for claims use, and some states are considering such bills.

Yet telematics also offers benefits for claimants. In a 2024 case in Illinois, telematics data helped a ride-share driver prove that she was not at fault in a collision, leading to a faster settlement. The data showed that the other driver had failed to yield, contradicting the other driver's statement. Without telematics, the claimant might have faced a prolonged dispute. Thus, while telematics can be used against claimants, it can also protect them. The key is ensuring transparency and consent, so that drivers understand how their data may be used. Insurers that adopt clear, upfront disclosure may build trust and reduce litigation.

Practical Takeaways for Regulators and Drivers

This case offers several lessons for regulators, insurers, and ride-share drivers. First, regulators should require clear disclosure of app-status coverage at the time of policy binding. The NAIC's model ride-share coverage act includes a provision for a 15-minute grace period after logout, but adoption has been slow. States that have not yet adopted the model act should consider doing so.

Second, regulators should consider capping reserve-to-paid ratios at 120% for personal auto liability claims. This would reduce the incentive for insurers to over-reserve and delay payment. Several states, including New York and Texas, have introduced such caps in recent legislative sessions, though none have passed as of mid-2026.

Third, insurers should be required to provide annual subrogation status reports to claimants. In this case, the claimant had no idea that a subrogation claim was being pursued until the settlement was reached. Transparency would allow claimants to understand the timeline and pressure insurers to resolve subrogation more quickly.

Finally, ride-share drivers should document their app status at the time of an accident, including screenshots of the app screen and timestamps. They should also review their personal auto policy to understand whether it covers business use. Many drivers assume they are covered during the gap period, but that assumption can be costly. The California court ruling in 2025 may eventually close the gap, but until then, drivers bear the risk.

This article is for informational purposes only and does not constitute legal, financial, or insurance advice. Readers should consult a qualified professional for guidance specific to their situation.