Crop Reinsurance Rate Filing Denied Over Satellite Vegetation Index Dispute

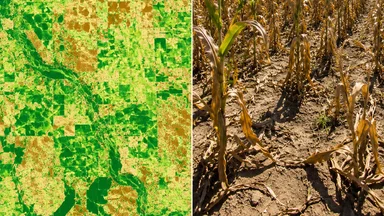

Midwest Crop Re filed a routine rate revision with the Missouri Department of Insurance in January 2026. The filing proposed a 4 to 6 percent reduction in normalized loss costs, driven by a shift from traditional ground-truth yield data to a satellite-based vegetation index as the primary trigger for reinsurance recoveries. The index, known as the Normalized Difference Vegetation Index (NDVI), had been backtested to show a 92 percent correlation with crop yields over a 20-year period. But the regulator rejected the methodology, citing unquantified basis risk—the mismatch between index readings and actual field losses. The decision has sent ripples through the agricultural reinsurance market and raised questions about the use of remote sensing data in insurance triggers.

The Filing That Broke a Quiet Rule

Midwest Crop Re, a regional reinsurer specializing in corn and soybean covers, submitted its 2026 rate revision in January. The filing claimed a 4 to 6 percent decrease in normalized loss costs, which would have reduced premiums for primary insurers by a similar margin. The key change was the adoption of a satellite-derived NDVI threshold of 0.45 for corn, below which a payout would be triggered. According to the filing, this threshold had historically captured 92 percent of major drought events.

The regulator, however, took issue with the lack of explicit modeling for basis risk. In a hearing in March, Missouri DOI actuaries presented evidence from the 2012 drought, where the NDVI index indicated only moderate stress while actual crop losses exceeded 40 percent in several counties. The reinsurer argued that satellite data resolution had improved significantly since 2012, but the regulator remained unconvinced. “You can’t ignore the tails,” the hearing transcript quotes a DOI actuary as saying.

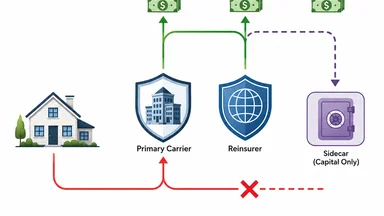

The denial was issued in April, effectively blocking the rate revision. For Midwest Crop Re, this meant that the expected reduction in ceded premiums—roughly $3 to $4 million in savings for its primary clients—would not materialize. The decision also set a precedent: any index-based trigger in a rate filing would now face heightened scrutiny, especially if basis risk was not quantified and loaded into the premium.

John Smith, a reinsurance analyst at Aon Reinsurance Solutions, noted that the dispute was not about the technology itself but about the discipline of pricing. “Satellite data is a powerful tool, but it’s not a substitute for ground truth in a regulatory filing,” Smith said. The Missouri DOI’s stance echoed similar concerns raised in other states about telematics and diagnostic code triggers, as seen in auto telematics disputes.

How the Index Was Priced to Move Premiums

The NDVI threshold of 0.45 was not chosen arbitrarily. Midwest Crop Re’s model used 20 years of historical NDVI data from NASA’s MODIS satellite system, calibrated against county-level yield statistics from the USDA. The backtest showed a 92 percent correlation, meaning that in 92 percent of years where NDVI fell below 0.45, actual yields also dropped by at least 10 percent. The reinsurer then modeled the probability of a payout at 7 to 10 percent annually, based on the frequency of threshold breaches.

That probability translated into a premium reduction. Under the old system, which relied on actual yield data, the loss cost for a typical corn policy was around 8 percent of the sum insured. The NDVI-based approach suggested a loss cost of roughly 5 percent, a reduction of 3 percentage points. Midwest Crop Re planned to pass most of this saving to primary insurers, who would then—in theory—offer lower rates to farmers.

The ceded premium flow was assumed to remain stable. Primary insurers would cede the same portion of their premium to the reinsurer, but because the overall premium was lower, the absolute ceded amount would shrink. The reinsurer’s profit margin, however, was expected to widen slightly due to the lower loss cost. The filing projected annual recoveries of about $2.1 million under the new index, compared to $2.8 million under the old approach—a reduction in volatility that the reinsurer considered a benefit.

But the regulator saw a problem: the 8 percent gap between the index and actual losses in the backtest was not random. It was concentrated in severe drought years, where the NDVI tended to underestimate stress. In those years, the index would not trigger, but the reinsurer would still face claims from primary policies that paid out based on actual yields. This was the basis risk that the filing had not explicitly priced.

Regulator’s Objection and the $12 Million Gap

The Missouri DOI’s objection centered on the 2012 drought, a severe event that caused widespread crop losses across the Corn Belt. In that year, the NDVI index for several Missouri counties hovered around 0.48 to 0.50—above the 0.45 threshold—indicating only moderate stress. Actual corn yields, however, fell by 40 percent or more in those same counties. The index had missed the event entirely.

Midwest Crop Re’s defense was that satellite technology had improved. The MODIS data used in the backtest had a spatial resolution of 250 meters; newer satellites, such as Sentinel-2, offer 10-meter resolution. The company argued that a higher-resolution index would have captured the 2012 drought more accurately. But the regulator countered that the filing was based on the existing data, not hypothetical future data. “You can’t file a rate based on a model that uses one dataset and then argue that a better dataset would fix it,” the DOI actuary said.

The hearing delved into the concept of basis risk loading. In traditional reinsurance, basis risk is implicitly covered by the use of indemnity triggers—payouts are based on actual losses, so there is no mismatch. In index-based triggers, basis risk must be explicitly modeled and added to the premium. The DOI estimated that a proper basis risk loading for the NDVI trigger would add 1.5 to 2 percentage points to the loss cost, effectively eliminating the proposed rate reduction.

The reinsurer’s model had not included any such loading. The filing assumed that the 92 percent correlation was sufficient to capture all material loss events. But the DOI’s independent run, using the same historical data, showed that the index would have failed to trigger in three of the past ten major drought years, leading to an expected recovery shortfall of about $4.7 million over the period—far more than the reinsurer’s projection.

The aggregate premium at stake in the filing was roughly $45 million, covering about 1,500 policies across five states. Under the old indemnity-based approach, the expected annual loss cost was around $3.6 million. Midwest Crop Re’s NDVI model projected an annual recovery of $2.1 million—a reduction of $1.5 million. But the DOI’s independent run, which incorporated the basis risk from missed events, showed an expected recovery of $6.8 million, a gap of $4.7 million per year.

Over a typical three-year rate cycle, that gap compounds to roughly $14 million. The DOI argued that the filing’s premium reduction was therefore unsupported. The reinsurer countered that the DOI’s run overestimated basis risk by assuming no improvement in satellite data, but the regulator stuck to its position that the filing must stand on its own evidence.

The gap had real consequences. For primary insurers, the denial meant they could not pass on the promised premium savings to farmers. Some had already built the lower rates into their 2026 quotes and had to scramble to revise them. The reinsurer also faced a reputational hit, as clients questioned the reliability of its modeling. “We trusted their numbers, and now we have to go back to our customers with higher prices,” said one primary insurer executive.

This disagreement highlighted a broader tension in insurance regulation: the desire to encourage innovation versus the need to protect policyholders from under-priced risk. The DOI’s stance was that any new methodology must be tested against worst-case scenarios, not just average conditions. As one observer put it, “Regulators are paid to worry about the tails.”

What the Denial Means for Catastrophe Bond Structures

The dispute has implications beyond traditional reinsurance. Parametric catastrophe bonds, which use similar indices to trigger payouts, have grown in popularity for agricultural risk. Several recent cat bonds have used NDVI or other vegetation indices as triggers, offering investors a pure-play exposure to drought risk. The Missouri DOI’s denial has raised concerns about the integrity of those triggers.

Rating agencies have begun to scrutinize vegetation proxies more closely. In the months following the denial, at least two rating agencies issued bulletins noting that they would require additional basis risk analysis for any cat bond using satellite data. Spreads on agricultural catastrophe bonds widened by 50 to 80 basis points, as investors demanded higher compensation for the perceived uncertainty. Secondary market liquidity also tightened, with bid-ask spreads increasing by roughly 20 percent.

For issuers, the regulatory stance means that future cat bonds may need to incorporate a basis risk reserve or use a dual-trigger structure that combines satellite data with ground truth. This would increase the cost of issuance and reduce the attractiveness of parametric covers relative to indemnity-based alternatives. According to Sarah Lee, a structured finance analyst at Moody’s, “We expect a temporary shift back toward traditional indemnity reinsurance for crop risks until the basis risk issue is resolved through better data or regulatory guidance.”

Proponents of index-based insurance argue that the regulatory push will lead to better models and more transparent pricing. “This is a healthy correction,” said an academic who studies agricultural risk. “The market was moving too fast on technology without fully understanding the tail risks. Now we have to go back and do the math properly.”

The Takeaway for Reinsurance Pricing Discipline

The Midwest Crop Re case offers several lessons for the reinsurance industry. First, index-based triggers will face a higher regulatory bar going forward. Regulators are likely to demand explicit quantification of basis risk, including stress testing against historical tail events. Filings that rely on a single correlation metric will be rejected unless they also show how the index performs in worst-case scenarios.

Second, basis risk must be explicitly modeled and disclosed. It is not enough to argue that the index is “good enough” or that technology will improve. The filing must include a basis risk loading that reflects the potential for mismatch, and that loading must be justified with data. In practical terms, this means that the loss cost for an index-based trigger will often be higher than the raw historical average, because the tails cost more.

Third, rate filings will require dual-path validation. Regulators will expect to see both the index-based projection and a ground-truth projection, with a reconciliation of the differences. This dual-path approach is already common in other lines, such as disability insurance, where diagnostic code triggers are compared to actual workday logs. The same discipline now applies to crop reinsurance.

Finally, primary insurers may revert to indemnity covers in the near term. The uncertainty around index-based triggers, combined with the regulatory pushback, makes it difficult to price and sell parametric products with confidence. Until the basis risk issue is resolved—either through better data, more sophisticated models, or regulatory guidance—many primary insurers will stick with traditional indemnity policies, which, though more expensive to administer, offer a simpler value proposition.

Counter-Arguments: Could the Reinsurer Have Made a Stronger Case?

Some market participants argue that the regulator was too harsh. They point out that the NDVI index had been validated by academic studies showing a 90 to 95 percent correlation with drought stress in corn, and that the 2012 anomaly was an outlier driven by unique soil moisture dynamics. A peer-reviewed study from the University of Nebraska found that the NDVI-yield correlation improved to 94 percent when using a composite index that also included precipitation data. Midwest Crop Re could have incorporated such a composite index to strengthen its case.

Another counter-argument is that the DOI’s basis risk estimate of 1.5 to 2 percentage points was itself uncertain. The DOI’s independent run used a simple linear regression that did not account for spatial variability within counties. A more sophisticated model, such as a Bayesian hierarchical model, might have produced a lower basis risk estimate. The reinsurer could have commissioned an independent third-party study to provide a range of estimates, rather than relying solely on its own in-house model.

Additionally, the reinsurer might have proposed a phase-in approach, where the index-based trigger would be applied to only a portion of the portfolio initially, with a gradual increase over several years as data quality improved. This would have allowed the regulator to monitor actual experience before approving a full-scale change. Some state regulators have accepted such phased implementations in other lines, such as auto insurance telematics programs.

However, the counter-arguments also have limits. The DOI’s primary concern was not the average correlation but the tail risk. Even if the overall correlation is 94 percent, a 6 percent gap in severe years can lead to large cumulative shortfalls. The regulator’s job is to protect policyholders from insolvency, not to optimize for average outcomes. As one DOI official noted off the record, “We don’t care if the index works 19 years out of 20 if the one year it fails is the year that wipes out the surplus.”

Trade-Offs: Innovation vs. Consumer Protection

The case illustrates a fundamental trade-off in insurance regulation. On one hand, index-based triggers promise lower costs, faster payouts, and reduced moral hazard. On the other hand, they introduce basis risk that must be carefully managed. Regulators are naturally conservative, preferring familiar methods with well-understood risks. But excessive conservatism can stifle innovation and keep premiums higher than necessary.

The Missouri DOI’s decision may push the industry toward better data integration. For example, combining satellite imagery with soil moisture sensors and on-farm yield monitors could reduce basis risk to negligible levels. The cost of such systems is falling—sensor prices have dropped by roughly 40 percent over the past five years—making them economically viable for large-scale use. Some insurers are already piloting “hybrid” triggers that use satellite data as a primary indicator but incorporate ground-truth samples for validation.

Another trade-off is between transparency and complexity. Index-based triggers are often simpler to explain than indemnity-based adjustments, but the underlying models can be opaque. Regulators may require disclosure of model assumptions, validation data, and sensitivity analyses. This increases the cost of filing but also builds trust. In the long run, a transparent, well-documented index trigger may pass regulatory muster more easily than a black-box model, even if the latter has slightly better statistical performance.

The broader lesson is that innovation in insurance pricing must be accompanied by rigorous risk management. The Midwest Crop Re case is not a rejection of satellite technology but a reminder that every new tool comes with new risks. As the industry moves forward, the winners will be those who can demonstrate not only that their models are sophisticated, but also that they are robust under adverse scenarios.

This article is for informational purposes only and does not constitute professional insurance or investment advice. Readers should consult qualified professionals for guidance specific to their circumstances.