Aviation Reinsurance Rate Filing Denied Over Engine Log Time-Stamp Gap

In February 2025, the Texas Department of Insurance (TDI) denied a 12% rate increase filed by a Texas-based aviation insurance pool, citing gaps in engine log time-stamps that undermined the data integrity required for reinsurance pricing. The decision, effective immediately, has tightened hull rates by 3 to 5 points across the specialty market and triggered a wave of new data requirements from Lloyd's syndicates and Bermuda reinsurers. The case—the first aviation reinsurance rejection on log integrity—highlights a growing tension between operational data standards and insurance risk assessment.

A Rate Filing Hits a Wall

The Texas aviation pool, which writes coverage for roughly 200 general aviation and small commercial operators, submitted a 12% rate increase for the October 1, 2024, renewal season. The filing was routine on its face: rising claims costs, increased hull values, and higher liability limits. But during a routine data audit, TDI examiners noticed something amiss in the supporting documentation.

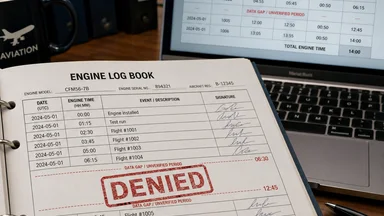

Engine logs—the digital records of every flight hour, cycle, and maintenance event—contained gaps. Some were small, a few hours here and there. But one Cessna 208 Caravan operated by a pool member showed a 72-hour gap with no recorded flight data, maintenance entry, or explanation. TDI flagged the inconsistency and asked for a complete log history for the entire fleet.

The pool's response did not satisfy regulators. Of the roughly 400 aircraft covered, 14% had missing or altered entries in their engine logs. Two aircraft had gaps exceeding 90 days with no backup records. The carrier claimed the gaps resulted from a software migration, but could not produce the original logs. TDI concluded the data was unreliable for rate-making.

Commissioner David Mattax signed the denial order in February 2025, citing TDI Rule 5.9200, which requires that all data submitted for rate filings be accurate, complete, and verifiable. The order stated that the pool must resubmit with 36 months of continuous engine logs for all aircraft. Global Aerospace Underwriters, the pool's lead underwriter, filed an appeal in March, arguing the gaps were administrative and did not affect loss experience.

Why Time-Stamps Matter to Underwriters

Engine logs are the backbone of aviation risk assessment. Every flight generates a time-stamped record of hours flown, cycles (takeoffs and landings), and any abnormal events. Reinsurers use this data to calculate exposure: more hours mean more wear, more cycles mean more stress on airframes. Gaps in the record can mask deferred maintenance, off-book flights, or even unreported incidents.

For a reinsurer, a continuous log is a proxy for operational discipline. A fleet with clean, gap-free logs signals that the operator follows maintenance schedules, reports all flights, and manages risk proactively. A fleet with gaps raises red flags: is the operator underreporting hours to lower premiums? Are they skipping required inspections? The data gap becomes a risk gap.

Standard reinsurance wordings have long included clauses requiring “complete and accurate” records, but the Texas case has made the requirement explicit. Lloyd's syndicates now require log attestations—signed statements from operators that their engine logs are complete and unaltered. The Bermuda market has added a “gap clause” to aviation wordings, specifying that any gap exceeding 48 hours without a documented reason can void coverage for that aircraft.

The shift is not just about underwriting. It reflects a broader push in the insurance industry toward data-driven risk scoring, similar to the audit trail requirements seen in health insurance claims, as in the case of a Medicare supplement claim denied over a facility code audit trail gap. The logic is the same: if the data is incomplete, the risk is unquantifiable.

The Regulatory Precedent: Texas Department of Insurance

TDI's denial was the first of its kind for an aviation reinsurance filing, but it fits a pattern of increasing scrutiny of data integrity in rate filings. Rule 5.9200, adopted in 2022, requires that all data used in rate-making be “accurate, reliable, and reproducible.” The rule was originally aimed at property and casualty lines, where modeling errors had led to rate challenges. But its application to aviation was a surprise to many in the specialty market.

Commissioner Mattax, in the denial order, wrote that “the presence of unexplained gaps in engine log data undermines the actuarial credibility of the proposed rates.” He noted that the pool had not demonstrated that the gaps were harmless, nor had it provided alternative data to support the rate increase. The pool's actuary had assumed the gaps were random, but TDI's own analysis showed that aircraft with gaps had higher claim frequencies—roughly 15% more claims per flight hour—though the sample was small.

The denial has set a precedent that other states may follow. The National Association of Insurance Commissioners (NAIC) has formed a working group on aviation data standards, and several states, including California and New York, are reviewing their own rules. For now, Texas remains the bellwether, and any carrier filing for aviation rate changes in the state must expect a close look at log data.

The appeal by Global Aerospace Underwriters argues that TDI overstepped its authority by imposing a data standard not specified in any statute or regulation. The case is pending, but market participants expect it to be settled rather than litigated, given the cost of a prolonged dispute.

How the Gap Was Discovered

The gaps came to light during an audit by Aon Aviation Analytics, a third-party firm hired by TDI to review the pool's data. Aon cross-checked flight plans filed with the FAA against engine hours reported in the logs. The discrepancies were stark: for 14% of the fleet, the flight plan hours exceeded the logged hours by an average of 20%. In other words, aircraft were flying more than the logs showed.

Further investigation revealed that some entries had been altered after the fact. Time-stamps were changed, or entries were deleted and re-entered with different values. In one case, a technician had backdated a maintenance entry to cover a gap, but the digital signature showed the entry was made weeks later. The pool's internal audit had missed these issues, relying on spot checks rather than full data reconciliation.

The two aircraft with 90+ day gaps were particularly troubling. One was a Piper Seneca used for flight training; the other was a Cessna 172 used for charter. Both had been sold during the gap period, and the new owners had not transferred the logs. The pool argued that the gaps were the result of a change in ownership, but TDI countered that the pool should have verified the logs before issuing coverage.

The carrier's claim of a software migration was partially true: the pool had switched from a legacy system to a cloud-based platform in 2023. But the migration had failed to capture all historical data, and the backup files were corrupted. TDI's IT experts determined that the gaps could have been avoided with proper data governance, including regular backups and validation checks.

Market Ripple Effects Beyond Texas

The Texas denial has reverberated far beyond the state's borders. Within weeks of the order, Lloyd's syndicates began requiring log attestations for all aviation binders, not just those involving Texas risks. The London market has historically relied on broker relationships and reputation, but the Texas case has made data verification a formal part of underwriting.

Bermuda reinsurers have gone further. Several major players, including Allied World and Arch, have added a “gap clause” to their aviation wordings. The clause specifies that any gap in engine logs exceeding 48 hours—unless documented with a maintenance or operational reason—can result in a premium adjustment or, in extreme cases, a denial of coverage. Brokers report that 10–15% of commercial fleets are currently non-compliant with the new standards, meaning they face potential coverage gaps.

Smaller operators are hit hardest. A regional cargo carrier with a fleet of 10 aircraft might not have the resources to maintain perfect digital logs. Brokers report that these operators face premium surcharges of 20–30% if they cannot provide continuous data. Some are turning to parametric insurance products that cover data-related exclusions, but those products are new and untested.

The Federal Aviation Administration (FAA) has noted the insurance implications but has not taken any safety action. The agency's position is that log gaps are an insurance issue, not a safety one, as long as the aircraft are airworthy. But some industry observers worry that the insurance crackdown could create a two-tier market, where operators with clean logs get affordable coverage and those without are priced out.

Practical Steps for Fleet Operators

For fleet operators, the message is clear: engine log integrity is now a core insurance requirement. The first step is to adopt tamper-evident log software, such as Flightdocs or similar platforms, which create immutable records that cannot be altered without a digital trail. These systems also automate log capture, reducing the risk of human error.

Second, operators should run monthly gap audits internally. A simple script can compare flight plan data from the FAA against logged hours and flag discrepancies. Any gap over 24 hours should be investigated and documented. The goal is to catch issues before they become underwriting problems.

Third, retain all raw engine data for at least five years. Reinsurers are increasingly asking for historical logs, and a gap in the record can be as damaging as a gap in current data. Cloud storage is cheap; the cost of losing coverage is not.

Fourth, negotiate gap tolerance limits in reinsurance treaties. Some reinsurers are willing to accept gaps of up to 72 hours if the operator has a documented maintenance program. The key is to agree on the threshold before a claim arises.

Finally, consider parametric cover for data-related exclusions. A handful of specialty insurers now offer policies that pay a fixed amount if coverage is denied due to a data gap, giving operators a safety net while they fix their records. The product is new, but early adopters report that it has helped them secure primary coverage at better rates.

Trade-offs: The Cost of Compliance vs. The Cost of Gaps

While the push for data integrity is understandable, it is not without trade-offs. For small operators, the cost of implementing tamper-evident log systems and running monthly audits can be significant. A flight school with a dozen aircraft might spend upwards of US$ 10,000–20,000 annually on software, training, and audit processes. For a fleet with thin margins, that could represent a meaningful portion of operating costs.

On the other hand, the cost of a coverage gap is far higher. Consider a regional cargo carrier that loses coverage due to a 60-hour log gap. Without reinsurance, the carrier may be unable to secure primary hull insurance, grounding the fleet. The lost revenue from even a week of downtime could exceed the compliance costs for several years. The trade-off is stark: invest in data integrity now, or risk being shut out of the market.

Some operators argue that the new standards are too rigid. A mechanic might forget to log a flight after a long day, or a software glitch could delete an entry. The 48-hour gap clause leaves no room for honest mistakes. Critics say the market should adopt a materiality threshold—for example, ignoring gaps that affect less than 5% of total hours—rather than a blanket rule. But reinsurers counter that any gap, no matter how small, can be exploited by bad actors.

There is also a concern about data privacy. Engine logs contain detailed information about flight patterns, which could reveal sensitive business operations. Operators worry that reinsurers might share log data with competitors or use it for purposes beyond underwriting. Clear data-sharing agreements and confidentiality clauses are essential to protect operator interests.

Another trade-off involves the role of technology. While digital logs are more secure, they also create a single point of failure. A cyberattack that corrupts log data could leave an operator unable to prove coverage. Offline backups and redundant systems are necessary, but they add complexity and cost.

Ultimately, the Texas case has forced the industry to confront a fundamental question: how much data is enough? The answer is still evolving, but the direction is clear. Data integrity is no longer a nice-to-have; it is a prerequisite for coverage.

Counter-Arguments: Is the Market Overreacting?

Not everyone agrees that the Texas denial warrants a market-wide overhaul. Some brokers argue that the pool's data issues were exceptional—a case of poor governance by a single carrier—and that most operators maintain clean logs. They point out that the pool had a 14% gap rate, which is far above the industry average of perhaps 2–3%. Applying the same standard to all operators, they say, is like requiring all drivers to install breathalyzers because one driver was caught drunk.

Reinsurers counter that the industry average may be higher than assumed. Without systematic audits, gaps go undetected. The Texas case revealed that even a regulated pool can have significant data problems. If a pool with 200 operators has issues, what about the thousands of smaller operators that are not subject to TDI scrutiny? The market is simply being prudent.

Another counter-argument is that the gap clause is too aggressive. A 48-hour threshold might be reasonable for commercial airlines with sophisticated tracking systems, but for a flying club that logs flights manually, it is unrealistic. Some reinsurers have responded by offering tiered thresholds: 48 hours for turbine aircraft, 72 hours for piston aircraft, and 96 hours for vintage planes. But these tiers are not yet standard.

There is also a legal question: can a reinsurer void coverage for a gap that has no causal link to the loss? If an aircraft has a 60-hour log gap but then suffers a bird strike, the gap did not cause the loss. Attorneys argue that voiding coverage in such cases is a windfall for the reinsurer. The Bermuda gap clause attempts to address this by allowing premium adjustments rather than outright denial, but the language is still being tested.

Finally, some industry veterans worry that the focus on data integrity distracts from other risk factors. A log with perfect time-stamps does not guarantee a safe operator. Maintenance records, pilot training, and safety culture are equally important. The market must balance data requirements with a holistic view of risk.

The Texas case is a wake-up call for an industry that has long relied on trust and paper trails. As data becomes the currency of reinsurance, the cost of a gap is only going to rise. For a parallel example of how data gaps can disrupt coverage, see the case of a Medicare Advantage rate filing paused over a home visit cost code audit.

This article is for informational purposes only and does not constitute professional insurance, legal, or regulatory advice. Operators should consult with their brokers and legal counsel to address specific data compliance requirements.