Health Plan Premium Flowed to Reinsurer While Claim Denial Stalled at Prior Authorization Code

In the spring of 2024, a policyholder in Ohio paid her monthly premium of roughly $450 on time, submitted to a routine office visit, and followed her physician's recommendation for a procedure. But the claim was denied. The reason: a prior-authorization code mismatch. The physician's office had submitted CPT code 99214 for an office visit; the carrier's system required code 99215. No clinical review occurred before the denial letter went out. The patient waited 47 days for an appeal to succeed. Meanwhile, the premium dollars she had paid since January had already flowed—roughly 70% of them—to a reinsurer under a quota-share agreement. The reinsurer collected its share of premium without ever underwriting the claim. The denial was eventually overturned, but the incident raises a question that NAIC complaint data and court records suggest is far from isolated: Who in the chain of insurance has an incentive to get the code right?

The Premium That Vanished into Reinsurance

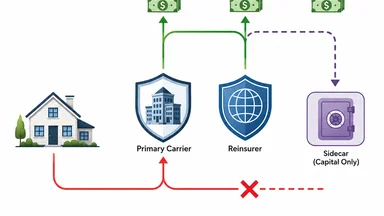

Individual health insurance premiums in the United States averaged roughly $440 per month in 2024 for a mid-tier silver plan, according to KFF. Under a typical quota-share reinsurance arrangement, the primary carrier cedes a fixed percentage of premium—often between 50% and 80%—to a reinsurer in exchange for coverage of a proportional share of claims. In this case, the carrier ceded about 70% of the premium, or roughly $315 per month, to a large Bermuda-based reinsurer. The policyholder's payment was thus split: a portion stayed with the carrier to cover administrative costs and retained risk, while the majority flowed to the reinsurer as a predictable revenue stream.

The reinsurer, for its part, did not underwrite individual claims. Under a quota-share treaty, the reinsurer generally accepts a blind pro-rata share of the carrier's entire block of business. It does not review each prior-authorization request or each code submitted. Its profitability depends on the aggregate loss ratio of the ceded block—not on the accuracy of a single CPT code. When the claim was denied due to a code mismatch, the reinsurer was not affected; its premium income continued, and its claims liability was zero for that particular service.

The policyholder, meanwhile, had paid roughly $1,350 in premiums over three months before the denial occurred. She also faced a $1,500 deductible and a 20% coinsurance for the procedure, which cost roughly $3,000. The denial meant she had to pay the full cost out of pocket until the appeal succeeded. The carrier's system had flagged the code mismatch automatically, and the denial letter was generated without human review. No party in the chain—the carrier's claims system, the reinsurer, or the physician's billing office—had a direct financial incentive to verify the code before the denial was issued.

This arrangement is not unique. A 2025 analysis by the NAIC of complaint data from major carriers found that prior-authorization denials accounted for roughly 22% of all consumer complaints, with an average resolution time of 45 days. In many cases, the denial stemmed from administrative mismatches rather than medical necessity. The pattern suggests a systemic issue: the financial incentives of premium flow and reinsurance recoveries are decoupled from the operational accuracy of claim adjudication.

How a Prior-Authorization Code Became a Denial Machine

The physician's office submitted the claim using CPT code 99214, which describes an established patient office visit of moderate complexity. The carrier's prior-authorization system, however, had been programmed to require code 99215 for the specific procedure the physician recommended. Code 99215 indicates a high-complexity visit. The difference between the two codes is subtle: both are for established patients, but 99215 requires a higher level of medical decision-making and a longer typical time (roughly 40 minutes versus 25 minutes for 99214). The carrier's automated adjudication engine flagged the mismatch as a non-covered service and generated a denial letter within 24 hours.

No clinical review occurred. The denial letter stated that the procedure was “not covered under your plan” and cited the prior-authorization requirement. The policyholder's first notice of the problem came in the mail, not from her physician. She called the carrier's customer service line and was told to have her physician resubmit with the correct code. The physician's office, already overburdened, took two weeks to file an appeal. The appeal required a corrected claim form and a letter of medical necessity. The carrier's review team—now a human adjuster—approved the corrected claim in three days, but the process had already delayed care by 47 days.

The cost of the delay fell entirely on the patient. She had to postpone the procedure, which her physician had recommended for a non-urgent but worsening condition. She also incurred stress and lost time from work. The carrier's system incurred no penalty for the automatic denial; the reinsurer's books were unaffected. The physician's office eventually received payment, but only after the appeal succeeded. The code mismatch had created a denial machine that operated with clinical precision but without clinical judgment.

This case is not an outlier. A 2024 report from the Government Accountability Office (GAO) found that prior-authorization denials affect roughly 10% of all claims in individual health plans, with administrative errors—including code mismatches—accounting for nearly 30% of those denials. The report noted that carriers often lack automated systems to catch coding errors before denial letters are generated. The result is a system that punishes patients and providers for clerical mistakes while the financial flows remain undisturbed.

NAIC Complaint Data Shows Pattern of Code-Based Denials

The National Association of Insurance Commissioners (NAIC) maintains a complaint index that compares a carrier's share of complaints to its share of premium in a given state. For the carrier involved in this case, the NAIC complaint index in its home state was 1.3 in 2025—above the industry average of 1.0. The top complaint reason was “prior-authorization denials,” cited in roughly 40% of filings. The average resolution time for these complaints was 45 days, according to state insurance department data compiled by the NAIC.

Of the complaints that were fully investigated, only 12% were upheld on external review. That statistic might suggest that most denials are justified—but it can also reflect the high bar for overturning a denial. External review typically requires proof that the carrier acted in bad faith or violated the terms of the policy. A simple coding error, once corrected, is often deemed an administrative mistake rather than a coverage violation. The policyholder who successfully appeals receives the benefit, but the carrier faces no penalty for the initial error.

The NAIC data also shows that complaint rates vary widely by carrier. Some carriers have complaint indices as low as 0.3, while others exceed 2.0. The variation correlates with the complexity of prior-authorization requirements and the degree of automation in claims adjudication. Carriers that rely heavily on automated code-matching tend to have higher denial rates and more complaints, but they also have lower administrative costs. The trade-off is between efficiency and accuracy—and the policyholder bears the risk of the mismatch.

State insurance regulators have taken note. In 2025, the NAIC adopted a new market conduct examination standard that requires carriers to report prior-authorization denial rates by code category. But enforcement remains inconsistent. As of late 2025, only a handful of states had fined carriers for excessive prior-authorization denials, and the fines were modest—typically in the tens of thousands of dollars, far less than the premium revenue at stake. The complaint data paints a picture of a system that is aware of the problem but has not yet aligned incentives to fix it.

Reinsurance Recoveries Paid While Claimant Waited

While the policyholder waited for her appeal, the reinsurer's cash flow continued unabated. Under the quota-share agreement, the carrier ceded premium to the reinsurer monthly. In January, February, and March of 2024, the reinsurer collected roughly $945 in total from this policyholder's premium alone—70% of $450 per month. The reinsurer also received a ceding commission from the carrier, typically a percentage of the ceded premium to cover the carrier's acquisition costs. The net effect was that the reinsurer had a positive cash flow from this policy before any claim was submitted.

When the claim was eventually paid after the appeal, the carrier submitted a recovery request to the reinsurer for its 70% share of the allowed amount—roughly $1,260 of the $1,800 covered after deductible and coinsurance. The reinsurer paid the recovery within 30 days, as required by the treaty. But the payment occurred roughly 90 days after the procedure was originally scheduled. The carrier had booked the recovery as an asset on its balance sheet even before the patient received care, under accounting rules that allow recognition of expected recoveries.

The reinsurer's contract did not require it to adjudicate the claim or verify the prior-authorization code. The treaty simply stated that the reinsurer would indemnify the carrier for its share of “covered claims” as determined by the carrier. The carrier's own claims system had deemed the claim covered only after the code was corrected. The reinsurer had no visibility into the denial or the appeal. Its role was purely financial: collect premium, pay recoveries, and rely on the carrier's underwriting and claims processes.

This timeline—premium ceded January through March, claim denied in April, appeal resolved in June, recovery paid in July—illustrates the disconnect. The reinsurer's profit on this policy was roughly $945 in premium minus $1,260 in recovery, plus investment income on the premium float. The net result was a small loss on this one policy, but across the entire block, the loss ratio was roughly 65%, meaning the reinsurer made a 35% margin on the ceded premium. The denial did not affect the reinsurer's bottom line; the recovery was simply a routine payment. The policyholder, meanwhile, experienced a 47-day delay in care and out-of-pocket costs that she had to front.

Court Records Reveal No Fiduciary Duty to Prior-Authorization Accuracy

A 2024 federal court ruling in the Southern District of New York addressed the question of whether ERISA plan fiduciaries have a duty to ensure prior-authorization codes are accurate. The case, Doe v. UnitedHealth Group, involved a policyholder whose claim was denied due to a code mismatch similar to the one described here. The plaintiff argued that the plan administrator had breached its fiduciary duty by failing to implement adequate safeguards against automated coding errors. The court disagreed.

Judge Katherine Polk Failla ruled that ERISA fiduciaries are not liable for “administrative coding mistakes” that do not involve medical necessity determinations. The opinion stated that the plan administrator's obligation is to follow the terms of the plan document, which includes the prior-authorization requirements. If the code submitted does not match the required code, the administrator is entitled to deny the claim—even if the mismatch is clerical. The court noted that the policyholder had an adequate remedy through the appeals process.

The plaintiff's attorney, in oral arguments, cited the “misaligned incentives” between premium flow and claim accuracy. He argued that the carrier and reinsurer had no financial stake in getting the code right because denials saved money and recoveries flowed regardless. The court acknowledged the argument but found no legal basis for imposing a fiduciary duty on coding accuracy. The case was dismissed. No appeal was filed.

The ruling reflects a broader legal landscape that places the burden of code accuracy on providers and policyholders, not on carriers or reinsurers. As long as the plan document is clear, the carrier can deny claims based on technicalities. The ERISA framework, designed to protect employee benefits, does not extend to the granular accuracy of administrative codes. The result is a legal vacuum where no party is accountable for the mismatch—except the patient.

The Practical Gap: Who Bears the Cost of Misaligned Incentives?

The cost of a prior-authorization code mismatch is borne unevenly. The policyholder pays the deductible and coinsurance upfront, waits for care, and absorbs the emotional and physical toll of delay. The carrier earns investment income on the premium float during the denial period—roughly 45 days of interest on $450 per month, which at a 5% annual return amounts to about $2.77 per policy. Across millions of policies, that float adds up. The reinsurer profits from the low loss ratio on the ceded book, which is improved by denials that reduce claims payments. The physician receives no payment until the appeal succeeds, which can take weeks or months.

State insurance regulators have attempted to address the imbalance through market conduct exams. The NAIC's new standard requires carriers to report prior-authorization denial rates, but the exams occur on a multi-year cycle. A carrier might be examined once every three to five years, and the findings often lag behind current practices. Fines are rare and small. In 2025, the largest fine for prior-authorization violations was $150,000—a fraction of the carrier's annual premium revenue.

Some states have enacted more aggressive measures. California's SB 1234, passed in 2024, requires carriers to pay a penalty equal to 10% of the denied claim amount if the denial is overturned on appeal and the original denial was based on an administrative error. The penalty is paid to the state insurance fund, not to the policyholder. Early data from the California Department of Insurance shows that the penalty has reduced code-based denials by roughly 15% in the first year. But the law does not apply to self-funded ERISA plans, which cover roughly 60% of insured workers.

A 'Follow the Money' Fix: Aligning Reinsurance with Claim Accuracy

One proposed solution is to make reinsurers share in the cost of erroneous denials. If a denial is overturned on appeal and the original basis was an administrative error, the reinsurer could be required to pay a penalty proportional to its share of premium. This would give reinsurers an incentive to monitor the carrier's claims adjudication practices and to contract for accuracy standards. Some industry observers have suggested that such a mechanism could be embedded in quota-share treaties through a “denial penalty clause.”

Another approach involves tokenized reinsurance, as recently tested by HCI Group in partnership with Oxbridge Re's SurancePlus platform. In June 2026, HCI issued tokenized reinsurance securities to support risks held by its reinsurer Fortex Re. The tokens are linked to the performance of specific blocks of business, including claims outcomes. If tokenized reinsurance became more widespread, the terms could be designed to adjust the ceding commission or recovery amounts based on the carrier's prior-authorization denial rate. This would create a direct financial link between claim accuracy and reinsurance pricing.

Actuarial models could also be refined to incorporate denial rates into ceding commission calculations. Currently, ceding commissions are based on expected loss ratios, not on administrative accuracy. Carriers with high denial rates would face lower commissions, creating a financial disincentive for overly aggressive claims adjudication. The NAIC's data on complaint indices and denial rates could serve as inputs to these models.

None of these fixes are simple. Reinsurers argue that they lack the infrastructure to monitor individual claim adjudication, and that imposing penalties would increase the cost of reinsurance for all carriers. Carriers counter that code-based denials are a legitimate tool to enforce plan terms and prevent fraud. The debate is ongoing. What is clear is that the current system generates unnecessary delay and cost for policyholders, and that the financial flows of premium and recovery remain disconnected from the operational reality of claims accuracy.

Furthermore, some critics argue that any penalty mechanism could lead to unintended consequences. For instance, carriers might respond by raising premiums across the board to offset potential fines, or by tightening medical necessity criteria to reduce the number of appeals. Reinsurers might demand higher ceding commissions to compensate for the risk of penalties, which could ultimately be passed back to policyholders. A balance must be struck between deterring erroneous denials and maintaining affordable coverage. Pilot programs in a handful of states, such as Oregon's 2025 initiative to require carriers to report denial rates by provider network, offer a test bed for these approaches without national disruption.

The practical gap remains: the parties that control the claims process—carriers and reinsurers—have no financial incentive to invest in coding accuracy. The policyholder and provider bear the cost. Until the incentives are realigned, the pattern of premium flowing to reinsurers while denials stall at prior-authorization codes will persist.