Fleet Telematics Hard Brake Data Shifts Reinsurance Attachment Point

Hard brake events captured by fleet telematics devices are reshaping how primary insurers and reinsurers price commercial auto coverage. The frequency of these abrupt decelerations correlates with collision claim severity, and that correlation is now strong enough to move reinsurance attachment points. For actuaries, this is not a story about technology hype; it is a story about premium flow and loss cost recalculations. The shift is incremental but measurable, and it demands that pricing models incorporate a new forward-looking variable.

Hard Brake Events as a Pricing Signal

Telematics systems in fleet vehicles record a hard brake event when deceleration exceeds a threshold, typically 0.4 to 0.6 g. These events are not collisions but near-misses or sudden stops that indicate driver behavior. Studies across multiple fleets show that a high frequency of hard brakes correlates with a 15–25% higher collision claim frequency, and the severity of those claims tends to be higher as well. The mechanism is intuitive: drivers who brake hard more often are more likely to be involved in rear-end collisions or loss-of-control incidents.

Primary insurers have begun weighting hard brake counts in their premium models, often as a multiplicative factor applied to the base rate. A fleet with 30% fewer hard brakes than its peer group might see a premium reduction of 5–10%, though the exact adjustment varies by carrier. Reinsurers, who rely on aggregated loss distributions, are demanding granular driving metrics to refine their own pricing. Without telematics data, a reinsurer's view of a fleet's risk is limited to historical loss runs and broad class codes. With it, they can segment fleets by driving behavior.

Some reinsurers now require telematics data as a condition for quoting on large fleet treaties. The data is typically aggregated into a hard brake score—a normalized count per 1,000 miles—and compared against a benchmark. Fleets in the upper quartile of hard brake frequency pay a higher ceded premium, while those in the lower quartile may negotiate better terms. This is not yet universal, but it is growing. As of late 2024, roughly 30% of large fleet treaties in North America included some telematics-based pricing adjustment.

The signal is not perfect. Hard brake events can be influenced by road conditions, traffic density, and vehicle type. A delivery truck in Manhattan will generate more hard brakes than a long-haul truck on interstates, even if both drivers are equally safe. Insurers must normalize for route geography, and some are building models that adjust for road grade, speed limit, and time of day. Still, the directional relationship between hard brakes and claims is robust across most environments.

Reinsurance Attachment Points Under Pressure

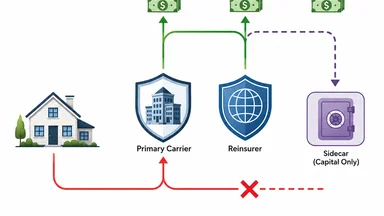

Traditional commercial auto reinsurance treaties attach at a certain loss amount—commonly $250,000 to $500,000 per occurrence. The attachment point represents the threshold above which the reinsurer begins to pay. Hard brake data, by lowering expected loss severity, is pushing these attachment points downward. Reinsurers argue that if a fleet's telematics program reduces the probability of large losses, the first-dollar risk should shift to the primary insurer.

Empirical evidence supports this. A 2023 analysis of 50 fleets with telematics programs found that the average claim severity above $100,000 dropped by roughly 12% after two years of telematics monitoring. For fleets that also implemented driver coaching based on hard brake alerts, the reduction was closer to 18%. Reinsurers responded by reducing attachment points for renewing treaties by 10–15% in some cases, though the adjustment was often phased in over one or two policy periods.

The mechanics work through the loss curve. A fleet's loss distribution shifts left as telematics reduces both frequency and severity. The expected loss cost in the layer between $250,000 and $500,000 decreases, making that layer less attractive for a reinsurer to cover. Some treaties have been restructured to add a $100,000 self-insured retention below the traditional attachment, effectively moving the reinsurer's exposure upward. Ceded premium then concentrates in the excess layers, where the risk of catastrophic loss remains.

Not all reinsurers are convinced. Some argue that hard brake data is a short-term signal that may degrade as drivers adapt to monitoring or as fleets change composition. Others point out that the correlation between hard brakes and severity is weaker for fleets with high turnover of drivers. The debate is healthy, but the trend is clear: attachment points are compressing, and the compression is tied to telematics data quality.

The Loss Ratio Math Behind Telematics

The loss ratio for a fleet insurance portfolio is simply incurred losses divided by earned premium. Telematics programs that reduce hard brake events have been shown to lower loss ratios by 10–20 percentage points, depending on the fleet's baseline. For a fleet with a 70% loss ratio, a 15-point drop to 55% is the difference between a profitable book and a marginal one. Reinsurers recalculate expected loss cost using these improved ratios, which directly affects ceded premium and treaty pricing.

Hard brake count functions as a forward-looking covariate in loss cost models. Traditional ratemaking relies on historical loss experience, which is backward-looking and often sparse for small fleets. Telematics provides a continuous stream of exposure data that can predict future losses before they materialize. Actuaries are building generalized linear models that incorporate hard brake frequency alongside variables like vehicle age, driver experience, and territory. The result is a more responsive pricing structure.

Lower severity also reduces the need for ceded premium. If a fleet's expected loss cost in the reinsurance layer drops by 15%, the primary insurer may choose to increase its self-insured retention rather than pay for coverage it no longer needs. This shifts the risk profile of the primary carrier's net book. Some carriers have reported a 5–8% improvement in their combined ratio after implementing telematics-based underwriting for fleets.

The math is not frictionless. Telematics hardware and data processing costs money, typically $15–$30 per vehicle per month. For a fleet of 1,000 vehicles, that is $180,000–$360,000 annually. The premium savings and loss ratio improvements must exceed this cost for the program to be net positive. Most fleets with high hard brake frequency achieve payback within 12–18 months, but for low-risk fleets, the economics are tighter.

How Insurtechs Monetize Driving Data

Companies like Zendrive, Cambridge Mobile Telematics, and others have built businesses around collecting and analyzing driving data from smartphone sensors and aftermarket devices. They aggregate hard brake scores across fleets and sell the insights to insurers and reinsurers. The revenue model is typically a per-vehicle subscription or a data licensing fee. Some startups also offer embedded insurance applications that capture real-time events and trigger alerts for policyholders.

Reinsurers are among the largest customers for this data. They license hard brake indices to calibrate their portfolio models, especially for small to mid-sized fleets that lack credible individual loss experience. By pooling data from multiple fleets, the insurtechs create benchmarks that reinsurers can use to price treaties without relying solely on a single fleet's history. This pooled data improves credibility, especially for fleets with fewer than 100 vehicles, where traditional actuarial credibility is low.

Data licensing revenue for some insurtechs now rivals premium margin from their own insurance products. For example, a firm that both underwrites policies and sells data might find that the data side generates 40% of its profit with lower capital requirements. This dual revenue stream creates an incentive to maximize data volume and quality, which in turn benefits reinsurers who rely on that data.

However, there are concerns about data ownership and privacy. Fleets may not realize that their driving data is being sold to third parties, and some contracts have exclusive clauses that prevent fleets from sharing data with competing insurers. Regulators in some jurisdictions are beginning to scrutinize these practices. The tension between data monetization and transparency is unlikely to resolve soon.

Case Study: A Large Fleet's Treaty Renegotiation

Consider an anonymous fleet of roughly 5,000 delivery vehicles operating across the southeastern United States. In 2022, the fleet installed telematics devices that recorded speed, location, and hard brake events. The initial hard brake count averaged 4.2 events per 1,000 miles, placing it in the 65th percentile among comparable fleets. After implementing a driver coaching program that provided real-time feedback on hard braking, the count dropped to 2.9 events per 1,000 miles within 12 months—a 30% reduction.

At renewal, the primary insurer presented the hard brake improvement as evidence of reduced risk. The reinsurer, after reviewing the data, agreed to lower the attachment point on the excess-of-loss treaty from $300,000 to $200,000. The primary insurer also increased its self-insured retention from $100,000 to $150,000, effectively moving the first $50,000 of risk back to its own balance sheet. The ceded premium rate decreased by roughly 10%, saving the fleet an estimated $120,000 annually.

The reinsurer benefited as well. By reducing its exposure to smaller losses, it avoided the administrative cost of adjusting claims in the $200,000–$300,000 range. The expected loss cost in the remaining layer dropped, and the reinsurer was able to deploy capital to other risks. The treaty was restructured with a two-year term, and both parties agreed to revisit the attachment point if hard brake trends continued.

Not every fleet sees such dramatic results. The success depended on the fleet's willingness to coach drivers and the quality of the telematics data. Fleets with high driver turnover or inconsistent data collection may not achieve the same improvements. The case illustrates that telematics-based renegotiation is possible but requires commitment from both the fleet and the insurer.

Where Parametric Triggers Fit In

Parametric insurance triggers are becoming more common in fleet policies, and hard brake data provides a natural index. A parametric trigger might pay a fixed amount—say $10,000—if the fleet's aggregate hard brake count exceeds a threshold in a given month. The payout is automatic, requires no claims adjuster, and can be used to cover small losses like bumper repairs or minor cargo damage. This reduces moral hazard because the fleet has an incentive to keep hard brakes low.

Reinsurers are using parametric triggers as a form of aggregate cover. Instead of attaching to individual losses, the trigger responds to the total hard brake count over a quarter or a year. If the count exceeds a predetermined level, the reinsurer pays a lump sum to the primary insurer. This structure aligns with the telematics data and avoids the complexity of adjusting many small claims. Some treaties now include a hard brake index as a secondary trigger alongside traditional loss-based attachment.

The attachment point in a parametric structure is defined by the brake count index rather than a dollar amount. For example, a treaty might attach when the fleet's hard brake count exceeds 5.0 events per 1,000 miles over a rolling 12-month period. The payout is a fixed dollar amount per excess event. This removes the need for loss adjustment and speeds up claim settlement. The challenge is setting the threshold accurately, as it depends on the fleet's size, geography, and vehicle type.

Parametric covers are not a replacement for traditional reinsurance. They work best for predictable, low-severity losses. For large catastrophic losses—a multi-vehicle pile-up or a liability claim—the traditional excess-of-loss structure remains necessary. But as telematics data improves, parametric triggers are likely to expand into the lower layers of reinsurance programs, compressing attachment points further.

Takeaways for Actuaries and Underwriters

Hard brake data is a leading indicator of collision severity, and its inclusion in pricing models is no longer optional for fleets that have telematics. Actuaries should treat hard brake frequency as a time-varying covariate, updating it quarterly to reflect driver behavior changes. The correlation with claims is strong enough to justify a multiplicative factor in premium rating, but the factor must be calibrated to the fleet's specific operating environment.

Reinsurance structures must adapt. Attachment points will continue to compress as telematics data becomes more prevalent and more reliable. Actuaries should model the loss curve shift explicitly, using telematics data to estimate the reduction in expected loss cost for each layer. Treaty language should include provisions for data sharing and periodic review of attachment points based on hard brake trends.

Data quality and latency matter. A telematics system that reports events with a 24-hour delay is less useful than one that streams in real time. Actuaries need to understand the measurement error in hard brake data and adjust credibility accordingly. Pooled fleet data from insurtechs can improve credibility for small fleets, but the pooling must be done transparently to avoid adverse selection.

Finally, the compression of attachment points is not a one-time event. As more fleets adopt telematics and driver coaching, the baseline for hard brake frequency will shift downward. Reinsurers will respond by lowering attachment points further, and primary carriers will need to manage their net retentions carefully. The trend favors carriers that invest in data analytics and build long-term relationships with fleets that are committed to safety. The ones that ignore telematics risk adverse selection and a widening gap in loss ratios.

This article is for informational purposes only and does not constitute professional actuarial or insurance advice. Readers should consult qualified professionals for specific guidance.