Medicare Advantage Rate Filing Pauses as Auditor Flags Home Visit Cost Code

In early June 2026, the Centers for Medicare & Medicaid Services (CMS) quietly halted the annual Medicare Advantage rate filing process. The trigger was an auditor's report flagging systematic misuse of a home visit cost code—a billing shortcut that had quietly padded risk-adjustment scores for years. The pause, which carriers must resolve by a fall deadline, has sent tremors through the health insurance market, exposing a fault line in how insurers document beneficiary acuity.

The Filing Freeze That Exposed a Coding Fault

CMS announced the pause on June 8, 2026, citing “concerns about the integrity of risk-adjustment data submitted by several Medicare Advantage plans.” The agency had received a preliminary audit from the Office of the Inspector General (OIG) showing that in roughly 40% of sampled claims, documentation for home visits did not support the severity of diagnoses recorded. The overpayment estimates, while not final, hover in the low billions of dollars—enough to rattle a market already sensitive to margin pressure.

Carriers now face a compressed timeline to re-file their rate submissions by the fall, likely with stricter documentation requirements. The freeze effectively suspends the 2027 rate approval cycle, delaying any premium adjustments and benefit changes that insurers had planned. For policyholders, this means uncertainty: open enrollment timelines may shift, and some plan features could be frozen until the CMS review is complete.

The audit findings align with a 2021 OIG report that flagged similar patterns in in-home health assessments, where insurers used visits to capture diagnoses that were not reflected in primary care records. The difference now is the scale: as Medicare Advantage enrollment has surged past 33 million beneficiaries, the financial impact of code inflation has grown proportionally.

Industry analysts note that the pause is unusual—rate filings are typically a procedural step, not a regulatory bottleneck. “This is a shot across the bow,” said one benefits consultant who declined to be named because their firm works with multiple carriers. “CMS is signaling that it will no longer accept passive oversight of home visit data.”

How Home Visit Codes Became a Profit Lever

Home visit cost codes—specifically, the in-home assessment codes HCPCS G0402 and G0438—were designed for frail, homebound beneficiaries who cannot easily travel to a doctor's office. The intent was to ensure that these patients' complex needs were captured in risk-adjustment models, so plans received adequate payment to care for them. But over the past decade, insurers expanded the use of these codes to routine check-ins for relatively healthy members, often through third-party vendors conducting annual wellness visits.

The result: risk-adjustment scores inflated by an estimated 15–20% for plans that aggressively used home visits. Since CMS payments are tied to these scores, the overpayment amounts are substantial. The CMS audit found that in many cases, the documentation did not support the diagnosed conditions—for example, a visit note might list diabetes without evidence of medication management or lab results.

Similar patterns appeared in the 2021 OIG report, which recommended that CMS strengthen oversight of in-home assessments. At the time, carriers argued that home visits improved care coordination and reduced hospitalizations. But the new audit suggests that the financial incentive to maximize scores overwhelmed clinical rationale.

“The codes were never meant to be a profit center,” said a former CMS actuary who now advises health plans. “But when you tie payment to documentation, you create a natural incentive to document as much as possible. The question is where the line is between proper coding and gaming the system.”

Market Reaction: Rates, Margins, and Consolidation Signals

News of the filing freeze hit markets immediately. Shares of UnitedHealth Group and Humana each fell roughly 3–5% on June 9 and 10, while smaller regional players like Health Care Service Corporation saw steeper declines. Analysts at several investment banks cut their 2027 margin forecasts for Medicare Advantage carriers by 1–2 percentage points, citing the risk of retroactive payment clawbacks and tighter documentation rules.

The margin pressure is especially acute for smaller regional plans that lack the data infrastructure to quickly re-file compliant rate submissions. Some may face cash-flow squeezes if CMS imposes payment holds during the review period. This dynamic is fueling consolidation chatter among mid-tier Medicare Advantage players, who see scale as the only hedge against regulatory risk.

In a separate but coincident event, W.R. Berkley Corp. announced on June 9 that its founder and executive chairman, William R. Berkley, had died at age 80. Berkley built the company from a startup in 1967 into a Fortune 500 property/casualty insurer. While not directly tied to Medicare Advantage, his passing adds succession uncertainty to a market already digesting the rate filing news. The company’s stock slipped 2% on the announcement.

For investors, the Medicare Advantage coding issue is a reminder that regulatory risk in health insurance is not limited to the Affordable Care Act exchanges. As one sector analyst put it, “The government is the biggest payer in health care, and when it changes the rules, the entire market reprices.”

Beyond the immediate stock moves, the filing freeze has also prompted a reassessment of the valuation multiples assigned to Medicare Advantage carriers. Historically, these plans traded at a premium to commercial insurers because of steady enrollment growth and predictable government funding. Now, analysts are questioning whether that premium is warranted. For example, a report from a major investment bank noted that if CMS imposes a 10% clawback on overpayments from the last three years, the impact on earnings per share for a typical large carrier could be in the range of $2–4 per share, or roughly 5–8% of current earnings. This has led to increased short interest in some health insurer stocks, as hedge funds bet on further downside.

The consolidation signals are also worth examining. In the past month, two regional Medicare Advantage plans have been rumored to be exploring sales. One, a plan based in the Midwest with roughly 200,000 members, has reportedly hired an investment bank to advise on strategic options. The other, a plan in the Southeast, has been approached by a private equity firm interested in acquiring its block of business. These moves reflect a belief that the regulatory environment will favor larger, more diversified carriers that can absorb compliance costs and spread risk across a broader membership base.

The D&O and Reinsurance Ripple Effect

The rate filing freeze has implications beyond Medicare Advantage margins. Directors and officers (D&O) liability insurers are watching closely. AM Best warned in a June 10 report that the D&O market is showing “warning signs” after four consecutive years of premium decline. Underwriting margins are shrinking, and a wave of regulatory actions—such as the CMS coding probe—could trigger claims against carriers for inadequate oversight or disclosure.

“If CMS determines that plans knowingly submitted inflated risk scores, shareholders could sue directors for breach of fiduciary duty,” said a D&O underwriter at a London-based specialty insurer. “That would be a shock to a market that has seen relatively few health-insurer D&O losses.” AM Best expects the D&O market to tighten in 2026, with higher rates and stricter terms for health insurers.

One concrete risk for D&O insurers is the possibility of securities class actions. In the aftermath of the CMS announcement, several law firms have already issued press releases announcing investigations into potential securities law violations by certain Medicare Advantage carriers. These investigations typically focus on whether the companies made false or misleading statements about their risk-adjustment practices. If a lawsuit is filed, the D&O insurance tower could be tapped for defense costs and potential settlement amounts, which may run into the tens of millions of dollars per case. For D&O underwriters, this means they must now carefully evaluate the coding practices of any health insurer they cover, and some have already begun adding exclusions for regulatory risk related to risk adjustment.

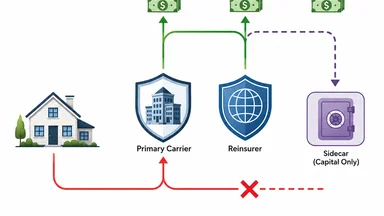

On the reinsurance side, new capital sources are emerging. On June 11, Oxbridge Re’s SurancePlus subsidiary announced a partnership with HCI Group to launch tokenized reinsurance securities on the Solana blockchain. The securities, tied to HCI’s Fortex Re program, offer synthetic returns based on catastrophe exposures. While initially focused on property catastrophe risk, the tokenization model could eventually extend to health insurance risks, providing alternative capital for carriers seeking to offload utilization volatility.

Catastrophe-linked securities have long been used for hurricane and earthquake risk. Their migration into health insurance is nascent but plausible, especially as investors seek uncorrelated returns. “Health risk is less well understood by capital markets, but the demand for yield is enormous,” noted a reinsurance broker familiar with the deal.

To understand how tokenized reinsurance might apply to health insurance, consider a hypothetical structure. A Medicare Advantage carrier could securitize a portfolio of home visit claims, transferring the risk that utilization spikes or coding audits lead to unexpected losses. Investors would receive a coupon tied to the performance of the portfolio, with the principal at risk if losses exceed a certain threshold. The appeal for carriers is that it provides a source of capital that does not require a traditional reinsurer's balance sheet. For investors, the returns are tied to health care utilization patterns, which have historically shown low correlation with equity and bond markets, making them attractive for diversification.

However, the complexity of health insurance risk—particularly regulatory risk—poses challenges for tokenization. Unlike hurricane risk, which can be modeled using historical weather data, the risk of a CMS audit or a change in coding rules is harder to quantify. This may limit the initial appetite for such securities to only the most sophisticated institutional investors. Still, the Oxbridge Re deal signals that the infrastructure for tokenized reinsurance is being built, and health insurers are taking notice.

Lessons from the Disparate Impact Repeal and Social Media Rulings

The CMS coding probe is unfolding against a broader regulatory backdrop that is reshaping how insurers use data. On June 11, the U.S. Department of Transportation rescinded its “disparate impact” civil rights regulation, which had prohibited practices that unintentionally harmed protected groups. The repeal, effective immediately, removes a key legal tool for challenging algorithmic bias in insurance pricing and underwriting.

For Medicare Advantage, the disparate impact rule had been cited in lawsuits alleging that risk-adjustment models disproportionately penalized plans serving minority beneficiaries. Its repeal could reduce litigation risk for insurers, but it also removes a check on potential discrimination in home visit coding practices. If home visits are concentrated among certain demographic groups, the coding inflation could exacerbate disparities in payment accuracy.

Separately, a California state court judge on June 11 denied motions by Google and Meta for a new trial after a jury found them liable for designing social media platforms harmful to young people. The ruling underscores a growing judicial willingness to hold companies accountable for algorithmic harms. Insurers that use algorithms to target home visits or prioritize certain diagnoses may face similar scrutiny if those algorithms produce biased outcomes.

The combination of these rulings suggests that while some civil rights enforcement is receding, the courts are stepping in—creating an uncertain liability environment for health insurers. As one legal analyst put it, “The risk is shifting from regulatory to litigative, and that can be harder to predict.”

Moreover, the repeal of the disparate impact rule does not eliminate all avenues for challenging discriminatory practices. The Equal Credit Opportunity Act, for example, still prohibits discrimination in credit transactions, and some states have their own fair lending laws that may apply to insurance. In addition, the Consumer Financial Protection Bureau has signaled an interest in algorithmic fairness, even as the Department of Transportation retreats. For Medicare Advantage carriers, this means they must still be vigilant about how their coding algorithms affect different populations. A plan that disproportionately schedules home visits for white, affluent members while neglecting minority communities could face reputational harm and potential state-level investigations.

What Policyholders and Agents Should Watch For

For Medicare Advantage beneficiaries, the rate filing freeze could mean changes to home visit coverage. Plans may narrow the scope of covered in-home assessments or require prior authorization to curb overuse. Policyholders who rely on home visits for chronic condition management should review their plan's benefits during open enrollment and consider whether alternative coverage, such as supplemental Medigap policies, might be more stable.

Agents need to verify network adequacy for home care services, as some plans may reduce vendor networks in response to the CMS scrutiny. “If a plan was relying on home visits to boost its star ratings, it may need to adjust its care coordination strategy,” said an independent agent who specializes in senior health. “That could affect quality scores and ultimately plan availability.”

Rate filing delays could shift open enrollment timelines for 2027. CMS has not yet announced new deadlines, but carriers are preparing for a compressed schedule. Agents should advise clients to watch for late notifications and to compare plans early, as some carriers may exit markets if the regulatory burden becomes too high.

Consumer complaints about denied home visits may rise as plans tighten documentation requirements. Beneficiaries who are denied a visit should request a detailed explanation and consider filing an appeal. The Medicare Rights Center has reported an uptick in calls about home visit denials since the audit news broke.

Finally, the star ratings system—which determines bonus payments to plans—may be recalculated to remove the effect of inflated risk scores. Plans that relied on home visit coding to improve quality metrics could see their ratings drop, affecting their competitiveness. Policyholders should check their plan's star rating history and consider whether a lower-rated plan still meets their needs.

Looking ahead, there are also potential legislative responses. Some members of Congress have already called for hearings on Medicare Advantage coding practices, and a bill has been introduced that would require CMS to audit a random sample of home visit claims each year. If passed, such legislation would add another layer of oversight and could lead to permanent changes in how home visits are reimbursed. For now, agents and policyholders should stay informed about these developments and be prepared for a more cautious regulatory environment.

Disclaimer: This article is for informational purposes only and does not constitute professional insurance, legal, or financial advice. Readers should consult qualified professionals for personalized guidance.