Professional Liability Claim Payout Stalled by Exclusion Clause Interpretation Dispute

A mid-sized engineering firm faced a negligence suit and sought indemnity under its professional liability policy. The carrier invoked exclusion clause 4.3, which bars coverage for claims arising from circumstances known before the policy inception. The payout froze. More than a year later, the dispute remains in court, with no end in sight. This case illustrates how a single clause can stall a claim, generate coverage litigation, and expose gaps in the claims-handling process.

A Claim Stalls on a Single Clause

The policyholder, a mid-sized engineering firm, held a claims-made professional liability policy with a limit of US$5 million. In late 2024, a client sued the firm for alleged design errors in a bridge project. The firm promptly notified its carrier, expecting coverage and defense. The carrier acknowledged the claim but, after a preliminary review, issued a reservation of rights letter citing exclusion 4.3: the policy did not cover claims arising from circumstances the insured knew or should have known before the policy period.

The carrier argued that internal emails from early 2024—months before the policy inception—showed the firm was aware of potential design flaws. The firm countered that the emails were routine project updates, not evidence of a known claim. The carrier froze all indemnity payments and refused to fund the defense beyond an initial US$100,000. The firm had to fund its own defense, racking up legal fees while the coverage question remained unresolved.

As of mid-2026, the coverage litigation is in its 18th month. The insured filed a declaratory judgment action in federal court seeking a ruling that the exclusion did not apply. Discovery has revealed a trove of internal communications, and expert testimony on industry standards for design review has been submitted. Summary judgment motions have been denied twice, with the judge citing genuine disputes of material fact over what the firm "knew" and when.

The dispute boils down to a single phrase: "known circumstances." The policy defined it as any fact or circumstance that a reasonable professional in the insured's position would believe could give rise to a claim. The insured's attorneys argue that the standard is too vague and that the carrier is using hindsight to second-guess routine project management. The carrier insists that the firm ignored clear red flags. The trial is set for the second quarter of 2027, according to the court docket.

The underlying lawsuit itself involves a bridge project in a coastal region, where the client alleges that design errors led to structural cracks and potential safety hazards. The client seeks damages exceeding US$10 million for repair costs and lost revenue. The engineering firm maintains that its designs met industry standards and that the cracks resulted from unforeseen soil conditions. This factual backdrop adds complexity to the coverage dispute, as the carrier may argue that the firm's awareness of soil instability before policy inception constituted a known circumstance.

How Exclusion Clauses Are Written – And Weaponized

Exclusion clauses are standard in professional liability policies. Many follow forms drafted by the Insurance Services Office (ISO), but larger insureds often negotiate manuscript language. Exclusion 4.3, in its common form, bars coverage for claims based on or arising out of any circumstance that the insured knew or could have reasonably foreseen might lead to a claim. The language is deliberately broad, giving carriers wide latitude to deny coverage when they suspect pre-existing knowledge.

Ambiguous phrases like "reasonably foreseeable" and "known circumstances" invite litigation. Courts in different jurisdictions have interpreted these terms inconsistently. Some require actual knowledge of a specific claim; others apply an objective standard of what a reasonable professional would anticipate. This uncertainty benefits carriers, who can deny coverage and force policyholders to sue to enforce their rights. For example, in a 2022 case from the Southern District of New York, a court found that an engineering firm's awareness of a client's dissatisfaction did not constitute knowledge of a claim, while a 2024 California appellate decision held that a contractor's internal risk assessment memos were sufficient to trigger a prior knowledge exclusion. Such splits create a patchwork of outcomes, making it difficult for policyholders to predict coverage.

Kathleen Faries, CEO of Artex Capital Solutions, noted in a mid-2026 interview that the growing complexity of insurance-linked securities and casualty lines is partly driven by such disputes. "Today's ILS market is significantly broader and more resilient," she said, "but complexity is rising." That complexity extends to policy language, where exclusion clauses become battlegrounds for coverage litigation.

Insurers draft exclusion clauses broadly to minimize underwriting risk. Policyholders and their brokers, however, often fail to scrutinize the language at renewal. A clause that seems standard may become a weapon when a claim arises. The result is that many disputes could be avoided with clearer drafting or negotiated carve-backs for routine project communications.

The Coverage Litigation Timeline – 18 Months and Counting

Coverage litigation is slow and expensive. In this case, the insured filed a declaratory judgment action in federal court roughly two months after the carrier issued its reservation of rights. The carrier responded with a motion to dismiss, arguing that the exclusion was unambiguous and that the insured's knowledge was clear from the emails. The court denied the motion, finding that factual disputes existed.

Discovery lasted nearly a year. Both sides deposed key employees and retained expert witnesses. The insured's expert, a professor of engineering ethics, testified that the emails were standard project management and did not indicate a belief that a claim was likely. The carrier's expert, a former professional liability adjuster, testified that the firm's failure to escalate the issue to senior management was itself evidence of knowledge. Additionally, a geotechnical engineer testified for the defense, arguing that the soil reports available before policy inception showed conditions that should have alerted the firm to potential design issues.

In early 2026, both sides moved for summary judgment. The judge denied both motions, ruling that a jury must decide what the insured knew and when. The trial is now set for the second quarter of 2027, more than two and a half years after the claim was first reported. By then, the insured's legal fees are expected to exceed US$1 million, with no guarantee of coverage.

This timeline is not unusual. A 2023 study by the Insurance Coverage Law Center found that the average coverage dispute over an exclusion clause took 22 months from filing to resolution, with 40% of cases going to trial. The costs often erode the policy limits, leaving little for the underlying claim. For the insured, the dispute becomes a drain on resources, distracting from the business.

Expert testimony plays a crucial role in these cases. In the current dispute, the insured's expert emphasized that the emails in question were part of a routine project update chain, where team members discussed potential design adjustments—common in complex engineering projects. The carrier's expert countered that the emails contained phrases like "urgent" and "needs immediate review," which a reasonable professional would interpret as red flags. The jury will have to weigh these conflicting interpretations.

Reserve Deficiencies and Market Pressure

While this dispute plays out, broader market trends are squeezing underwriting margins. AM Best recently flagged adverse loss development on accident years 2023 and 2024 for the directors and officers (D&O) liability line, warning that reserve deficiencies could signal trouble ahead. The same dynamics affect professional liability, where premium declines have compressed margins even as claim frequency and severity rise.

Reserve deficiencies occur when carriers set aside too little money to pay future claims. In a hard market, carriers may under-reserve to show profitability, only to find later that claims cost more than expected. This case illustrates the problem: the carrier's initial reserve for the claim was US$500,000, but after 18 months of litigation, the defense costs alone have exceeded that amount. The carrier has since increased the reserve to US$2 million, but the gap may widen if the case goes to trial.

p>Market discipline is expected to remain for Florida reinsurance heading into 2026, according to Fitch Ratings, but the casualty lines face different pressures. The D&O market remains profitable, but reserve deficiencies on older accident years could erode that profitability. For professional liability, the combination of broad exclusion clauses and aggressive claim denials may be a symptom of deeper underwriting problems.Some industry observers argue that carriers are using exclusion clauses to compensate for inadequate pricing. If premiums are too low, carriers can deny more claims to preserve margins. Policyholders, in turn, face higher premiums and narrower coverage at renewal. The cycle reinforces itself: tighter language leads to more disputes, which increase costs, which lead to higher premiums.

Data from the Professional Liability Underwriting Society shows that the average cost of defending a coverage dispute over an exclusion clause has risen by roughly 15% annually over the past five years, driven by increased discovery demands and expert fees. This trend pressures both carriers and policyholders to resolve disputes earlier, but the complexity of prior knowledge issues often prevents early settlement.

What the Policyholder Should Have Done Differently

In hindsight, the policyholder could have taken several steps to avoid or mitigate this dispute. A pre-loss audit of exclusion triggers would have identified the "known circumstances" clause as a potential risk. The firm could have documented its risk awareness protocols, showing that it had a formal system for flagging potential claims. Without such documentation, the carrier could argue that the firm was willfully blind.

Broker negotiation of a "prior knowledge" carve-back might have narrowed the exclusion. Some carriers offer manuscript language that excludes from the bar any circumstances that were reported to management but not deemed likely to result in a claim. The insured's broker did not seek such language, perhaps because the standard form seemed acceptable at the time. However, negotiating broader coverage may increase premiums, and some carriers refuse to modify standard forms. Policyholders must weigh the cost of additional premium against the potential cost of a coverage dispute.

Policyholders also have options regarding policy form selection. Claims-made policies cover claims reported during the policy period, but they are vulnerable to prior-knowledge exclusions. Occurrence policies cover incidents that happen during the policy period, regardless of when the claim is made, but they are less common for professional liability. Some insurers offer hybrid forms that combine features of both, but these often come with higher premiums and complex trigger language.

Early notification, even for uncertain claims, is critical. The firm waited several weeks after receiving the client's demand letter before notifying the carrier. That delay gave the carrier grounds to argue that the firm was aware of the problem earlier. Prompt notification, coupled with a detailed explanation of why the firm believed the claim was not covered by the exclusion, might have changed the carrier's assessment.

The Real Cost of a Disputed Payout

The direct costs of the dispute are easy to quantify: legal fees, expert witness costs, and lost management time. But the indirect costs can be larger. The insured's business reputation suffers when clients learn that coverage is in dispute. Third-party plaintiffs in the underlying negligence suit wait years for resolution, and their patience may wear thin. Some plaintiffs may be more inclined to settle if they see the insured struggling to fund its defense.

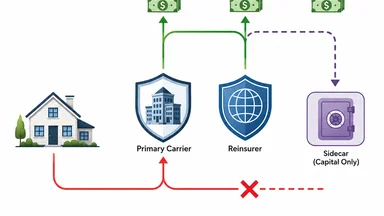

Reinsurance attachment points shift as the dispute drags on. The carrier's reinsurance treaty may have an aggregate limit or a per-claim deductible. If the carrier pays defense costs, those costs may erode the deductible, making the reinsurer liable for a larger share. Reinsurers, in turn, may impose stricter terms on the carrier at renewal, including narrower coverage or higher premiums.

The insurance-linked securities (ILS) market, which increasingly invests in casualty and specialty lines, is watching these disputes closely. As Kathleen Faries noted, the ILS market is growing more complex, and casualty structures are attracting interest. But the complexity of exclusion clause litigation is a risk factor that investors must price. Some ILS funds have begun to exclude policies with certain manuscript exclusions from their portfolios.

For the policyholder, the dispute may ultimately cost more than the policy limit. If the jury finds that the exclusion does not apply, the carrier will pay the underlying claim and defense costs, but the insured will have spent years distracted and damaged. If the jury finds for the carrier, the insured faces an uninsured liability that could bankrupt the firm. Either way, the cost of the dispute is a drain on the industry.

Takeaways for Risk Managers and Brokers

This case offers several lessons for risk managers and brokers. First, review exclusion language at every renewal, not just when a claim arises. The "known circumstances" clause is standard, but its scope can vary. Ask the carrier for examples of what would trigger the exclusion. If the carrier cannot give clear examples, the language may be too vague and should be negotiated.

Second, model "worst-case" litigation scenarios before a claim occurs. What would happen if the carrier denied coverage? How much would defense cost? How long would litigation take? The answers may prompt the insured to purchase higher limits or negotiate a broader coverage form. Some carriers offer optional coverage for "known circumstances" that are disclosed at inception.

Third, engage coverage counsel before a claim is reported, not after. A coverage lawyer can review the policy language and advise on how to present the claim to avoid triggering exclusions. In this case, the firm might have avoided the dispute if it had framed its notification differently, emphasizing that the emails were not evidence of a known claim.

Fourth, track the statute of limitations for bad faith claims. If the carrier unreasonably denies coverage, the policyholder may have a bad faith claim. The deadlines vary by state, but they are often shorter than the underlying statute of limitations. A bad faith claim can recover extra-contractual damages, including emotional distress and punitive damages, but it requires proof that the carrier acted unreasonably.

Finally, market discipline demands tighter wording. As the D&O and professional liability markets face reserve deficiencies and premium declines, carriers will look for ways to limit their exposure. Policyholders who accept broad exclusion clauses without scrutiny will pay the price when a claim arises. The time to push back is at renewal, not after the claim is denied.

But there is a trade-off. Negotiating broader coverage—such as narrowing the prior knowledge exclusion—often comes at a cost. Carriers may demand higher premiums or impose sub-limits for certain exposures. Some carriers refuse to modify standard forms altogether, forcing policyholders to choose between accepting the exclusion or seeking a different carrier. Risk managers must evaluate whether the additional premium is worth the potential reduction in coverage disputes, and whether the market offers viable alternatives.

As the industry evolves, one question remains: will the growing frequency of exclusion clause disputes push carriers to adopt clearer language, or will the ambiguity persist as a strategic tool? The answer may determine the future of professional liability coverage.

Disclaimer: This article is for informational purposes only and does not constitute legal or professional advice. Policyholders should consult with qualified legal counsel and insurance professionals regarding their specific circumstances.